Questions about what businesses and organizations can do to minimize negative effects on the environment, take affirmative action on human rights and sustainable development have already been raised in various global forums in light of the recent societal and environmental issues. To address them, governments around the world are introducing laws and regulations to hold companies accountable for their actions.

According to a Gartner survey, 87% of business leaders expect to increase their investment in sustainability over the next two years. The International Trade Center (ITC) reports that sales of sustainable goods have increased by almost 85% during the past five years.

Similar to how Germany introduced the Supply Chain Due Diligence Act (Lieferkettensorgfaltspflichtengesetz, LkSG), the European Commission (EC) recently approved the new CSRD (Corporate Sustainability Reporting Directive), which will motivate businesses in the EU to work toward their sustainable goals by publishing regular reports on their sustainability activities.

Sustainable procurement and enabling sustainability across their supply chains thus become inevitable for businesses. According to EcoVadis’ Sustainable Procurement Barometer, 61% of procurement executives believe that social challenges will have a strong influence on procurement strategies going forward.

In this blog post, we’ll explore:

- What is the EU Corporate Sustainability Reporting Directive (CSRD)?

- Which companies are affected?

- What does it mean for your organization?

- The role of sustainable procurement in achieving EU-CSRD compliance.

- How can businesses use technology to successfully address the challenges of sustainability reporting?

What is Corporate Sustainability Reporting Directive (CSRD)?

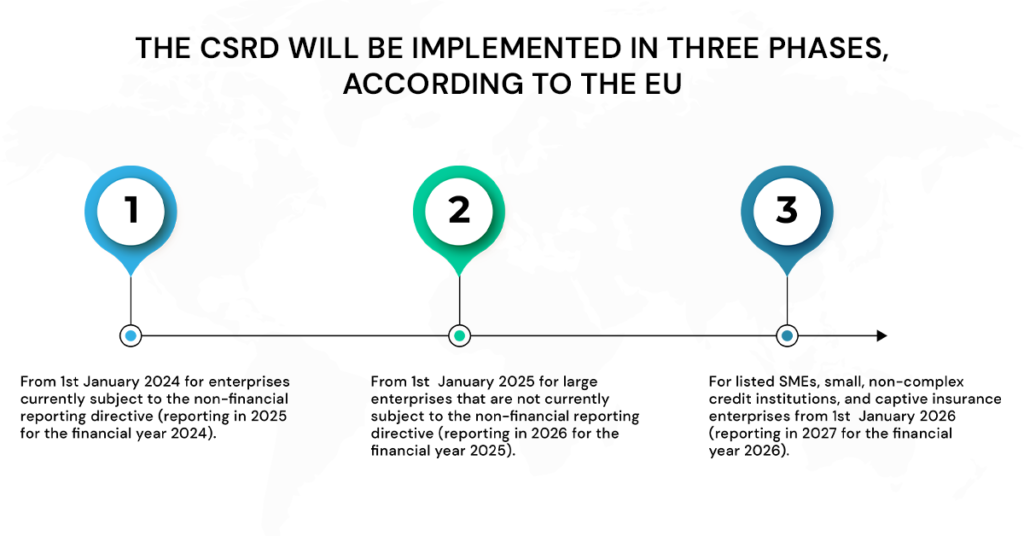

To assist investors, customers, political leaders, and other stakeholders in evaluating a company’s non-financial performance, the European Parliament enacted the Corporate Sustainability Reporting Directive (CSRD) on November 10, 2022. The standards governing the social and environmental data that businesses are required to provide have been updated and strengthened by this new directive. The EU has announced that the CSRD would be implemented in three stages:

-

- From 1st January 2024 for enterprises currently subject to the non-financial reporting directive (reporting in 2025 for the financial year 2024).

-

- From 1st January 2025 for large enterprises that are not currently subject to the non-financial reporting directive (reporting in 2026 for the financial year 2025).

-

- For listed SMEs, small, non-complex credit institutions, and captive insurance enterprises from 1st January 2026 (reporting in 2027 for the financial year 2026).

The new regulation will guarantee that stakeholders and investors have access to the data they need, to evaluate the investment risks associated with climate change and other sustainability-related concerns. Additionally, it will foster a culture of openness on how businesses affect both the environment and people. Finally, standardizing the required information will help businesses in minimizing reporting expenses over the long term. For example, CSRD can simplify the process for asset managers and investment companies to obtain ESG company data to ensure their compliance with reporting requirements under the EU Taxonomy and SFDR (Sustainable Finance Disclosure Regulation).

Which companies are affected?

All companies that meet at least two of these three criteria are subject to the CSR directive:

-

- The company’s total assets are €20 million or more,

-

- The company’s net sales are €40 million or more,

-

- The company employs at least 250 people or more.

All listed companies are subject to the requirement as well. Only microenterprises that fall under the criteria of having net sales of no more than €700,000, a financial statement of €350,000, and don’t have more than 10 employees on average per year are exempted from this law. To be considered a microenterprise, at least two of these three requirements must be satisfied.

What does it mean for your organization?

With CSRD being the new directive that establishes the framework for reporting, the organizations subject to it will be obliged to adhere to the European Sustainability Reporting Standards (ESRS) in terms of the disclosures required.

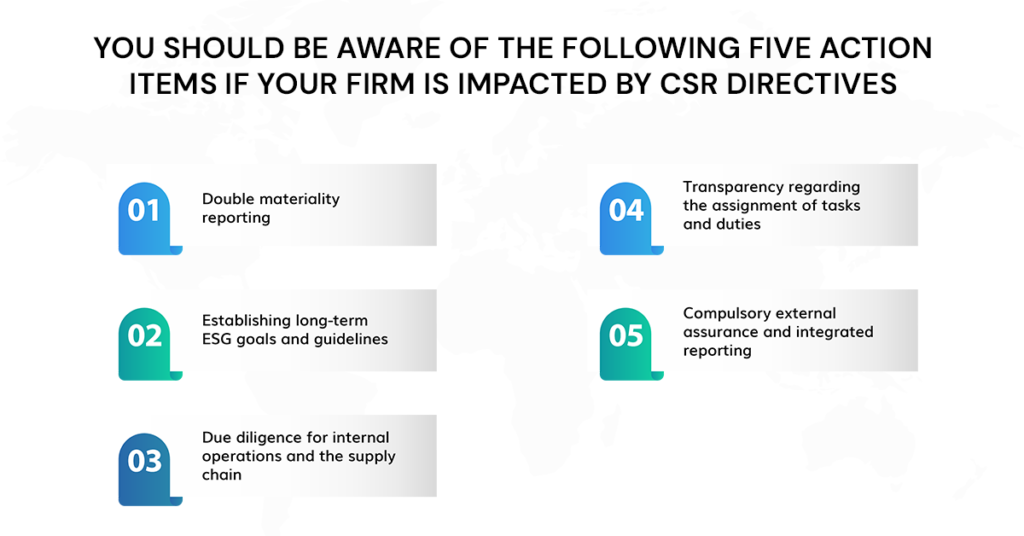

If your organization is affected by CSR Directives, you should be aware of the following five action points:

1. Double materiality reporting

‘Double materiality’ refers to the dual reporting obligations requirement from the companies in which they have to report on their influence on traditional materialities, such as the impact of their operations on sustainability issues as well as the need to disclose the risks they face from factors such as climate change or lack of resources, etc.

2. Establishing long-term ESG goals and guidelines

Companies are required to establish specific ESG goals and report on their development each year under the CSRD. As a result, the emphasis on sustainability is now required and must be incorporated into the company’s long-term vision and strategy as well as its internal policies.

3. Due diligence for internal operations and the supply chain

Businesses are required to account for and audit the effects of their internal operations and production methods. This also holds for how their supply chain partners’ actions affect them. Companies can thus no longer cover up any unethical behavior or environmental damage.

4. Transparency regarding the assignment of tasks and duties

According to the new EU-CSR directive organizations must specify who is in charge of setting ESG goals and tracking their achievement, as well as which divisions within the business are in charge of each. Companies need to determine which other partners are also accountable for implementing ESG initiatives.

5. Compulsory external assurance and integrated reporting

The annual report must include the sustainable targets and performance related to the targets in addition to ESG reporting that complies with the requirements endorsed by the European Commission. The data must then be audited by a third-party external auditor.

The role of sustainable procurement in achieving EU-CSRD compliance

As discussed above, the EU-CSRD regulations broaden the scope and raise the bar for sustainability requirements. This will necessitate significant changes by businesses to ensure the sustainability of their supply chains. As a result, coming to terms with them can pose complicated challenges for businesses, especially for those with less evolved supply chain sustainability measures.

However, by putting Sustainable Procurement practices into place, businesses can analyze CSR performance across their supplier ecosystem through effective supplier screening and management processes. It takes into account how the company’s supplier sourcing strategy may affect the economy, society, and the environment in addition to their potential to affect the cost and quality of the materials sourced.

This gets us to discuss the two strategies of sustainable procurement for CSRD:

1. Product-based strategy

Using an organization’s supply chain to build a product or service while evaluating its own and its suppliers’ environmental records is the focus of this method. For strategic and commercial objectives, this approach is used to comprehend the influence of a product or service. Additionally, this method offers a thorough record of the supplier’s process.

2. Supplier-based strategy

In this strategy, the supplier’s CSR approach and policy are analyzed, evaluated, and checked for conformity with your CSR criteria. This is an intriguing method since you can evaluate the supplier’s effects on the environment and societal dangers. With this strategy, you can encourage other companies to adopt more sustainable practices and enhance the entire supply chain process, which can be perceived as having a beneficial influence.

How can businesses use technology to successfully address the challenges of sustainability reporting?

As this new directive necessitates the collection, cleansing, and categorization of massive amounts of data on sustainability, technologies such as cloud-based strategic sourcing software, S2P suite or supplier management software (SXM or SRM) can play pivotal roles in managing supplier data through supplier management automation. It collects and processes information about the suppliers while analyzing the associated risks. It also helps businesses to integrate sustainable practices in the sourcing and supplier selection process and ensure that the organization has a more holistic view of sustainability risks before actually entering into a contract with the supplier.

Additionally, the best integrated strategic sourcing software comes with procurement analytics tools and reporting capabilities that enable businesses to assess KPIs using simple dashboards and generate reports in various formats. This makes it easier for businesses to report to both internal and external audiences on social compliance, human rights, and sustainability performances.

Conclusion

The journey to EU-CSRD reporting has just started. The EU aims to ensure that businesses not only adhere to directives but also actively embrace environmental transformation by integrating global sustainability frameworks with financial and non-financial performances. So, it’s now or never to start getting ready for your CSRD requirements! Make an appointment with a MeRLIN Sourcing expert to see how our solution can help you improve compliance with the law.